Solution :

Preferred Common

Non cumulative and non Participative 12,600 67,400

Cumulative and non participative 37800 42200

Cumulative and participative 47876 32124

Current Stock Out Standing

Common stock at the rate 50 5100 shares 255000

Preferred stock 7% at the rate 100 1800 shares 180000

Cumulative the annual dividend on the preferred stock

Preferred stock dividend (180000 x 7%) 12600

Dividend Arrears to preferred stock (12600 x 2) 25200

Non cumulative and non participative

Preferred Common Total

Current year 12600 12600

Arrears 0 0

Common stock 67400 67400

Total dividend 12600 67400 80000

Cumulative and non participative

Preferred Common Total

Current year 12600 12600

Arrears 25200 25200

Common stock 42200 42200

Total dividend 37800 42200 80000

Cumulative and participative

Preferred Common Total

Current year 12600 12600

Arrears 25200 25200

Common stock (255000 x 7%) 17850 17850

Balance dividend pro data 10076 14274 24350

Total dividend 47876 32124 80000

Working notes :

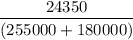

Amount for the participation = 80000-(12600+25200+17850) = 24350

Rate of participation =

= 5.5977%

= 5.5977%

Participating dividend:

Preferred stock = 18000 x 5.5977% = 10076

Common stock = 255000 x 5.5977% = 14274

Total participating dividend = 24350