Answer:

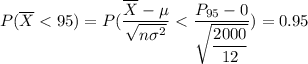

the 95th percentile for the sum of the rounding errors is 21.236

Explanation:

Let consider X to be the rounding errors

Then;

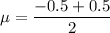

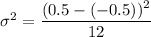

where;

a = -0.5 and b = 0.5

Also;

Since The error on each loss is independently and uniformly distributed

Then;

where;

n = 2000

Mean

Recall:

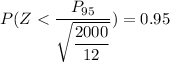

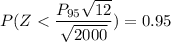

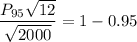

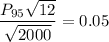

For 95th percentile or below

From Normal table; Z > 1.645 = 0.05

the 95th percentile for the sum of the rounding errors is 21.236