Answer:

a) Probability: 0.5488

b) Probability: 0.3012

c) Probability: 0.0907

d) Probability: 0.2476

Explanation:

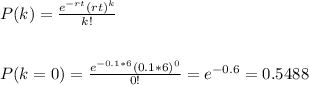

a) We can model this as a Poisson process, with parameter r=0.1.

We have to calculate the probability that no claim is made in 6 months.

The probability that the dealership will wait at least 6 months until the next claim is 0.5488.

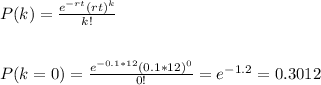

b) In this case, t=12 months.

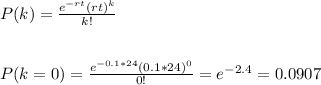

c) In this case, t=24 months

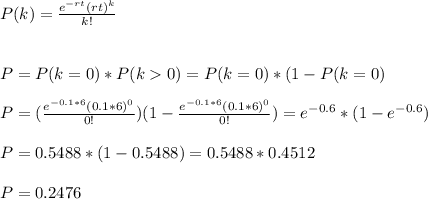

d) In this case, we have to multiply the probability that there is no claim in the first 6 months (k=0, t=6) and the probability that there is more than one claim in the next 6 months (k>0, t=6).

As the Poisson process is memoryless, the probabilitiies are independent of past events and can be calculated that way.