Answer:

Explanation:

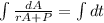

This is a separable differential equation. Rearranging terms in the equation gives

Integration on both sides gives

where

is a constant of integration.

is a constant of integration.

The steps for solving the integral on the right hand side are presented below.

Therefore,

Multiply both sides by

By taking exponents, we obtain

Isolate

.

.

Since

when

when

, we obtain an initial condition

, we obtain an initial condition

.

.

We can use it to find the numeric value of the constant

.

Substituting

for

for

and

in the equation gives

in the equation gives

Therefore, the solution of the given differential equation is