Answer:

c.negative

True, by definition since the variance take in count the differences around the mean squared, then we can't have a negative value for a sum of square values.

Explanation:

We need to remember that the variance is a measure of dispersion for a dataset respect to a measure of central tendency called the mean. The mean is defined as:

And the population mean is given by:

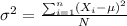

The population variance is defined by:

And the sample variance is defined as:

Now if we analyze the options we have this:

a.zero

False, if all the values are the same then the mean would be the same to the values and the difference between each value and the mean would 0 and indeed the variance would be 0.

b.larger than the standard deviation

False, if the population standard deviation is

then the variance would be

then the variance would be

and as we can see is higher than the standard deviation

and as we can see is higher than the standard deviation

c.negative

True, by definition since the variance take in count the differences around the mean squared, then we can't have a negative value for a sum of square values.

d.smaller than the standard deviation

False, if the population standard deviation is

then the variance would be

then the variance would be

and as we can see is lower than the standard deviation

and as we can see is lower than the standard deviation