0 Comments

Answer:

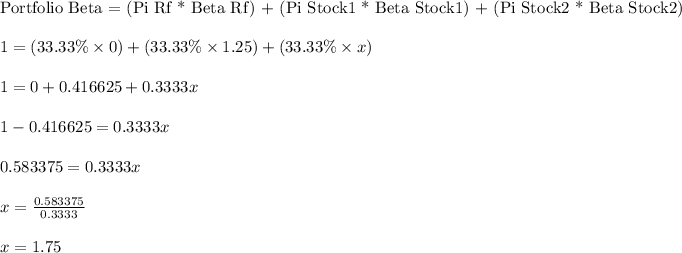

The answer is "1.75"

Step-by-step explanation:

The portfolio is equally weighted with three parts, which each weighs 33,33%. The risk-free asset (Rf) is available worldwide and beta 0 is given for the market portfolio.

9.4m questions

12.2m answers