Solution :

a). At the break even units, the total contribution margin = fixed expenses

We know that : (Selling price - variable cost) x units sold = fixed expenses

i.e. (20-14)x = 225,000

6x = 225,000

x = 37,500

Therefore, the number of units sold, x = 37,500

So, the break even analysis = 37,500 x 20

= 750,000

b).

= 30%

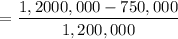

The Breakeven sales =

= 750,000

c).

= 37.5%

d). Units needed :

units

units

Therefore, the sales required = 62,500 x 20

= 125,000