menu

QAmmunity.org

Login

Register

My account

Edit my Profile

Private messages

My favorites

Register

Ask a Question

Questions

Unanswered

Tags

Categories

Ask a Question

Find the total amount in the compound interest account $10000 is compounded semiannually at a rate of 11% for 20 years. (Round to the nearest cent.)

asked

Jan 10, 2023

27.6k

views

3

votes

Find the total amount in the compound interest account $10000 is compounded semiannually at a rate of 11% for 20 years. (Round to the nearest cent.)

Mathematics

college

LingYan Meng

asked

by

LingYan Meng

6.6k

points

answer

comment

share this

share

0 Comments

Please

log in

or

register

to add a comment.

Please

log in

or

register

to answer this question.

1

Answer

5

votes

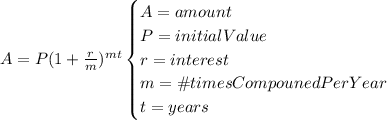

The compound interest formula is:

Therefore:

Sean Bannister

answered

Jan 17, 2023

by

Sean Bannister

8.0k

points

ask related question

comment

share this

0 Comments

Please

log in

or

register

to add a comment.

Ask a Question

Welcome to QAmmunity.org, where you can ask questions and receive answers from other members of our community.

8.8m

questions

11.4m

answers

Other Questions

How do you can you solve this problem 37 + y = 87; y =

What is .725 as a fraction

i have a field 60m long and 110 wide going to be paved i ordered 660000000cm cubed of cement how thick must the cement be to cover field

Write words to match the expression. 24- ( 6+3)

A dealer sells a certain type of chair and a table for $40. He also sells the same sort of table and a desk for $83 or a chair and a desk for $77. Find the price of a chair, table, and of a desk.

Twitter

WhatsApp

Facebook

Reddit

LinkedIn

Email

Link Copied!

Copy

Search QAmmunity.org