0 Comments

Answer:

Following are the solution to this question:

Step-by-step explanation:

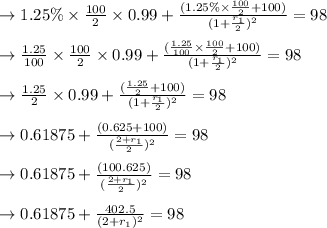

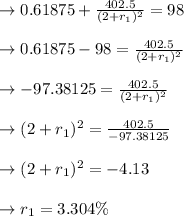

Assume that will be a 12-month for the spot rate:

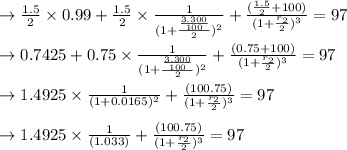

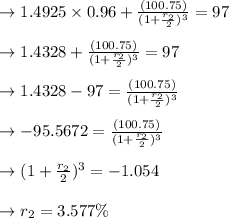

Assume that will be a 18-month for the spot rate:

to solve this we get

9.4m questions

12.2m answers

will be a 12-month for the spot rate:

will be a 12-month for the spot rate:

will be a 18-month for the spot rate:

will be a 18-month for the spot rate:

will be a 18-month for the spot rate:

will be a 18-month for the spot rate: