Answer:

The optimal Hedge Ratio is 0.7305.

Explanation:

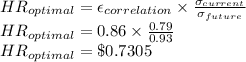

Optimal Hedge ratio is given as

Here

- HR_optimal is the Hedge Ratio for the next 6 months which is to be calculated.

- ε_correlation is the correlation coefficient relating the assets and futures contract whose value is give as $0.86.

- σ_current is the standard deviation of the semiannual changes of the wheat which is given as $0.79

- σ_future is the standard deviation of the changes in the future over the same time period which is given as $0.93

So the Hedge Ratio is given as

So the optimal Hedge Ratio is 0.7305.